Getting your insurance company to pay for roof replacement requires understanding your policy, proper documentation, and strategic navigation of the claims process. But here's what most homeowners don't know: sometimes, filing a claim can hurt you more than help you.

At Greater Midwest Exteriors, we've helped thousands of Midwest homeowners successfully navigate roof damage insurance claims over our 30+ years in the roofing industry. This comprehensive guide walks you through every step, from understanding your homeowners insurance policy to working with insurance adjusters and — crucially — knowing when NOT to file a claim.

The Critical First Decision: Should You Even File a Claim?

The most important rule: Never call your insurance company asking them to "send someone to check your roof". This automatically files a claim on your record, even if you don't get a penny.

The RIGHT approach:

- Call a professional roofing company for inspection FIRST.

- Determine if the damage meets insurance thresholds.

- If it does, contact your insurance company to file.

When NOT to File a Roof Insurance Claim

Sometimes, filing a claim can hurt you more than help you:

Don't file when:

- The damage is minor (e.g., fewer than 8-10 hail hits per 100 sq. ft.).

- The cost to repair is close to or less than your deductible.

- You have a high deductible (1-5% of your home's value).

- The damage is only cosmetic and doesn’t impact function or safety.

- You’re not planning to sell your home, and the damage isn’t getting worse.

The "zero pay claim" risk: Filing for insufficient damage results in a denied claim that stays on your insurance record permanently. This makes future coverage harder to obtain and can increase premiums, just like bad marks on your credit report.

Real example: A Naperville homeowner found 3-4 hail hits on their roof after a storm. Filing would have resulted in a denied claim on their record. Our advice: wait and monitor. If damage worsens or they decide to sell, they can reassess.

When You Should File a Claim

Clear indicators for filing:

- Extensive visible damage (10+ hits per 100 sq. ft. on multiple roof slopes)

- Missing shingles from high winds

- Damaged roof accessories (vents, flashing, gutters)

- Interior water damage or leaks

- Planning to sell your home (the damage will show up in the buyer's inspection)

Quick Action Checklist: First 48 Hours After Roof Damage

Immediate steps (do this now):

- Call a local roofing contractor first: You can call Greater Midwest Exteriors at (630) 463-7663 for a professional assessment BEFORE filing a claim.

- Document from the ground level: Take photos of visible damage from safe vantage points (let professionals handle roof-level documentation).

- Prevent further damage: Emergency tarps, remove standing water to prevent mold growth.

- Save all receipts: Emergency roof repair costs are often reimbursable.

- Know your deductible and coverage type: Critical for decision making.

⚠️ Don't do this:

- Don't call the insurance company asking for an inspection (this files a claim automatically).

- Don't climb on your damaged roof — this is dangerous, and you may miss critical damage details.

- Don't attempt professional-level documentation yourself — leave technical assessment to experienced contractors.

- Don't sign anything with door-to-door contractors who aren't reputable roofing contractors.

- Don't admit fault or acknowledge normal wear issues.

Understanding Your Homeowners Insurance Policy in Illinois and Surrounding States

Before making any decisions about filing a roof claim, you must understand what your insurance covers for your roof. Most Chicagoland homeowners carry HO-3 policies, which provide "open perils" insurance coverage for your dwelling structure.

What Insurance Covers for Roof Replacement

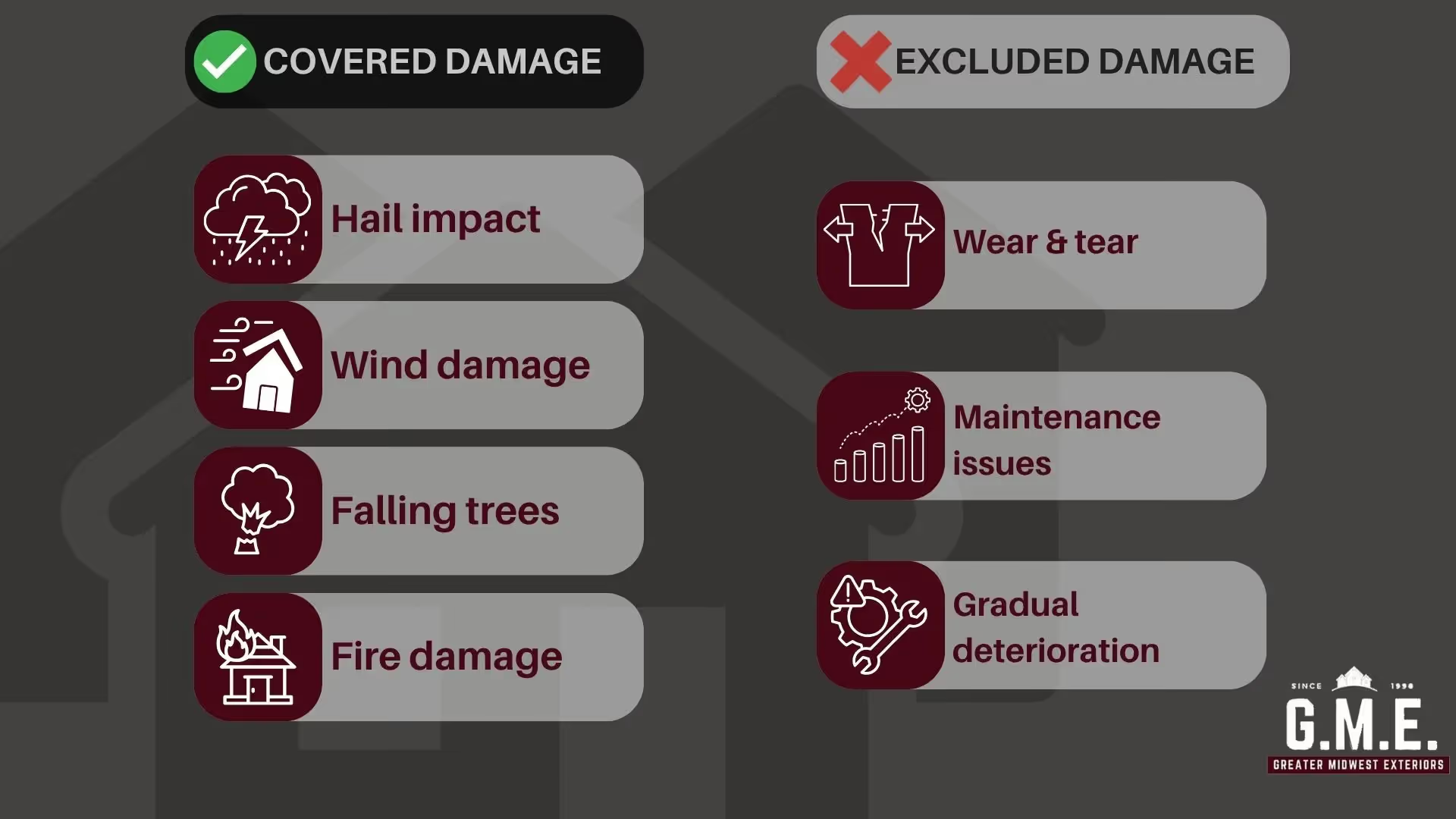

Storm damage from severe weather (common in our area):

- Hail damage: Illinois sees over 100 hail events annually, often causing missing shingles and extensive damage.

- High winds: Chicago's wind patterns can exceed 70 mph, leading to roof damage requiring repair coverage.

- Ice dam damage: Common in Wisconsin and Michigan winters, and can cause mold growth if not addressed.

- Fallen tree damage: From severe thunderstorms requiring immediate roof repair.

- Snow load damage: Heavy Midwest winters causing structural issues beyond normal wear.

The Critical Difference: Replacement Cost Value (RCV) vs. Actual Cash Value (ACV) Coverage

Understanding whether you have a Replacement Cost Value policy dramatically affects whether insurance will pay the full cost of your brand-new roof.

Real example from our experience: Last year, we helped a Naperville homeowner with a $25,000 roof replacement. With Replacement Cost Value coverage, they only paid their $1,500 deductible when the insurance company approved their claim. Their neighbor with ACV coverage on the same storm damage paid $11,000 out of pocket due to depreciation.

Replacement cost value policy (RCV):

- Insurance pays the full cost for a brand-new roof

- No depreciation is deducted regardless of the roof's age

- The two-payment system reduces the immediate financial burden

- It’s the best option when you need insurance to pay for a complete replacement

Actual cash value (ACV):

- Deducts depreciation based on the roof’s age and normal wear

- Much higher out-of-pocket financial burden

- It’s a common limitation for roofs over 15 years

- May not provide adequate repair coverage for older homes

Understanding Your Deductible Structure

This is critical (it catches homeowners by surprise):

- Flat deductibles: $500, $1,000, $2,500 fixed amount.

- Percentage deductibles: 1-5% of your home's insured value.

Real example: A homeowner thought she had a $1,000 deductible but discovered it had been changed to 1% of her home’s value — now $3,500 instead of $1,000. This completely changed whether filing the claim made financial sense.

GME's Professional Assessment Process

During our 30+ years of insurance work in the roofing industry, we've learned that proper assessment prevents costly mistakes with your roof claim.

Why Professional Assessment Comes First

Have GME inspect before filing your roof claim:

- We determine if the damage meets the insurance company's thresholds.

- We know what insurance adjusters look for during the insurance claim process.

- We provide an unbiased assessment on whether to file or not file.

- We protect you from getting a "zero pay claim" on your record.

Our professional assessment process:

- Comprehensive roof evaluation: All asphalt shingles, materials, and components.

- Damage threshold analysis: Does it meet the "10x10 test" adjusters use?

- Cost vs. deductible analysis: Is filing worthwhile financially?

- Record impact consultation: How will this affect your insurance history?

The "10x10 Test" Insurance Adjusters Use

What adjusters look for: Insurance adjusters typically draw 10-foot by 10-foot squares on major roof slopes and count hail hits. They generally need to see:

- 8-10+ impact marks within the 10-foot by 10-foot area on at least one major slope

- Evidence on multiple roof slopes

- Damage to roof accessories (vents, flashing, gutters)

If your roof doesn't meet these thresholds, filing usually results in denial.

Essential Documentation for Valid Claims

Photographic evidence:

- Wide shots show overall roof damage patterns from severe weather.

- Close-ups of hail impacts and missing shingles on asphalt shingles.

- Interior water damage and stains show extensive damage.

- Damaged roof accessories (vents, gutters, flashing).

Supporting documentation:

- National Weather Service storm reports confirming severe weather and high winds.

- Professional roofing company inspection (GME provides this).

- Maintenance records (proving good upkeep, not normal wear).

- Emergency roof repair receipts for repair coverage.

💡 GME pro tip: We provide comprehensive documentation packages that insurance companies trust. Our professional reports ensure legitimate claims get approved while protecting you from filing weak claims that get denied.

When Filing Makes Sense: GME's Step-by-Step Process

Step 1: Professional Assessment Confirms Claim Viability

Before we recommend filing, we verify:

- The damage exceeds insurance company thresholds

- Repair costs significantly exceed your deductible

- Evidence clearly shows storm causation vs. normal wear

- Your coverage type makes it financially beneficial to file

Step 2: Contact Your Insurance Company (Only After Professional Assessment)

What to say: "I'm reporting roof damage to my roof from [specific date’s] severe weather. I need to file a roof claim and schedule an insurance adjuster inspection".

Information you'll need:

- Policy number and policy details

- Date and time of severe weather event

- A brief roof damage description confirmed by a professional inspection

- Your contact information

Get your roof claim number — use this for all future communications.

Step 3: Schedule GME to Attend Your Insurance Adjuster Meeting

Why does this matter for your insurance to pay? Insurance adjusters work for your insurance company, not you.

Having our professional roofing company present ensures:

- All roof damage and missing shingles are properly identified

- Technical roofing industry issues are correctly explained

- Nothing gets overlooked that could affect the claim approval

- Fair scope and insurance estimate pricing discussions occur

Step 4: Navigate the Insurance Adjuster Inspection

What our professional roofing company does:

- Present professional roof damage documentation

- Explain why certain repair methods are necessary

- Ensure all storm damage is noted in the insurance estimate

- Advocate for proper materials and code compliance

Maximizing Valid Claims: The GME Advantage

Understand Insurance Payouts When Your Claim Gets Approved

For a replacement cost value policy (two-payment system):

- Initial payment: Actual cash value minus deductible.

- Final payment: Recoverable depreciation after work completion.

- Timeline: Must complete work within 180 days to receive full cost.

Example from recent GME project: Aurora homeowner — $18,000 roof replacement.

- Initial payment: $8,500 (ACV minus $1,500 deductible).

- Final payment: $8,000 (recoverable depreciation).

- Total out-of-pocket: $1,500 deductible only.

Supplemental Claims (Normal for Legitimate Damage)

Most roof projects require supplemental claims if:

- Extensive hidden damage was discovered during the tear-off

- Code compliance upgrades are needed for a brand-new roof installation

- Structural repairs are needed that go beyond basic roof repair

- Additional materials are needed beyond the original insurance estimate

GME's Track Record: We successfully obtain supplements on 85% of insurance jobs, averaging an additional $3,200 in covered work.

Special Scenarios: Borderline Damage Decisions

The "Forever Home" vs. "Planning to Sell" Decision

Forever home strategy — If you never plan to sell and the damage isn't worsening:

- Consider monitoring instead of filing immediately

- This avoids a claim on your record

- It also avoids the deductible payment

- The risk is that the damage could worsen over time

Planning to sell strategy — Even minor hail damage will show up in buyer's inspections:

- File a claim now while the storm causation is clear

- Address issues before they become negotiating points

- Protect your sales transaction

Percentage Deductible Scenarios

When high deductibles make claims uneconomical. For example, $20,000 roof replacement with 2% deductible on $300,000 home:

- Deductible: $6,000

- Insurance pays: $14,000

- Your cost: $6,000

…versus paying $20,000 out of pocket.

Sometimes the math doesn't work, especially for borderline damage.

When Insurance Denies Claims: Appeal Strategies

Common Denial Reasons We Overcome

"Pre-existing condition" denials:

- We provide maintenance records proving proper care.

- Weather data confirms storm timing vs. damage discovery.

- Professional assessment distinguishes storm damage from normal wear.

"Insufficient damage" denials:

- We document damage that meets insurance thresholds.

- We provide evidence of functional impacts beyond cosmetic issues.

- We demonstrate code compliance requirements.

"Cosmetic only" denials:

- We show how "cosmetic" damage affects roof function.

- We document granule loss patterns indicating impact damage.

- We explain how the damage will progress without repair.

GME's Appeal Success Rate

Our results when insurance initially denies:

- 78% of legitimate denials overturned on appeal

- Average additional recovery: $8,500

- Typical timeline: 30-45 days for claim approval on appeal

Illinois, Wisconsin, Indiana & Michigan Specific Considerations

State-Specific Regulations

Illinois:

- 2-year statute of limitations for roof claims

- Strict contractor licensing requirements

- Anti-fraud enforcement protects homeowners

Wisconsin:

- Enhanced wind/hail insurance coverage requirements

- Specific ice dam repair coverage provisions

- Different depreciation calculation methods

Indiana & Michigan:

- Varying deductible structures in homeowners' insurance policies

- Different code compliance requirements

- Regional weather pattern considerations

Local Weather Patterns We Know

Chicago area challenges:

- Lake effect weather intensifies storm damage

- Freeze-thaw cycles accelerate the deterioration of asphalt shingles

- High winds from prairie exposure are causing missing shingles

- Urban heat island effects require specialized materials

Choosing the Right Roofing Contractor: Red Flags vs. Professional Service

Storm Chasers to Avoid

Warning signs after severe weather:

- Door-to-door solicitation immediately after storms

- Out-of-state license plates and temporary presence

- Pressure for immediate decisions about filing claims

- Offers to waive deductibles (illegal in most states)

- Promises that "everyone in the neighborhood is getting approved”

The "spaghetti approach" problem: Some contractors use the "throw it against the wall and see what sticks" method, encouraging claims for minimal damage, hoping for favorable adjusters. This puts homeowners at risk for zero-pay claims.

The GME Difference as Your Trusted Partner

Our insurance expertise:

- 30+ years of legitimate insurance work in the Chicagoland

- We tell you NOT to file when the damage is insufficient

- Established relationships with regional insurance adjusters

- 99% customer satisfaction rate with ethical practices

- A+ BBB rating with zero fraud complaints

Our honest assessment process:

- Thorough inspection within 24 hours of roof damage

- Honest recommendation — file or don't file based on evidence

- Professional documentation only for viable claims

- Insurance adjuster support for approved claims only

- Long-term warranty backing on all completed work

Real GME Assessment Stories

Case Study 1: Orland Park, IL — Claim Recommended

Situation: Severe weather hailstorm caused extensive damage to the 10-year-old roof.

Assessment: 15+ hits per 100 sq. ft., damaged accessories, clear storm causation.

Recommendation: File a claim immediately.

Result: Full replacement cost value coverage approved ($22,000).

Homeowner savings: $20,500 after $1,500 deductible.

Case Study 2: Naperville, IL — Claim NOT Recommended

Situation: High winds caused 3-4 missing shingles.

Assessment: Minimal damage, easily repaired, wouldn't meet adjuster thresholds.

Recommendation: Don't file — repair out of pocket ($800).

Result: No claim on record, avoided potential denial.

Homeowner savings: Protected insurance history worth thousands in future premiums.

Case Study 3: Aurora, IL — Borderline Damage, Strategic Decision

Situation: Moderate hail damage, homeowner planning to sell in 2 years.

Assessment: Damage present but minimal, would likely be approved.

Recommendation: File a claim to avoid issues during the sale.

Result: Claim approved for $15,000 after initial pushback.

Home sale impact: No negotiation issues, clean inspection report.

Your Decision Framework: To File or Not to File

Use This Checklist

File the claim if:

- Damage exceeds 8-10 hits per 100 sq. ft. on multiple slopes

- Roof accessories are damaged (vents, gutters, flashing)

- Repair costs exceed deductible by $3,000+

- You're planning to sell within 5 years

- Damage affects roof function, not just appearance

- Professional assessment confirms storm causation

DON'T file the claim if:

- Damage is minimal or borderline

- Repair costs barely exceed the deductible

- You have a high percentage deductible (over $5,000)

- It's a "forever home", and the damage isn't worsening

- Professional assessment suggests likely denial

- Recent claim history makes you vulnerable

The Financial Analysis

Calculate your break-even point:

- Repair cost estimate: $______

- Your deductible: $______

- Net insurance benefit: $______

- Risk of claim on record: Consider future impact

If the net benefit is under $2,000 and the damage is minimal, consider waiting.

Your Next Steps: Making the Right Decision

If You Have Current Roof Damage

Step 1: Professional assessment (within 24-48 hours)

- Call GME: (630) 463-7663

- Get a free inspection and honest recommendation

- We’ll document the damage properly if the claim is warranted

Step 2: Financial analysis

- Confirm your exact deductible amount

- Understand your coverage type (RCV vs. ACV)

- Calculate the true net benefit of filing

Step 3: Make an informed decision

- File only if damage clearly meets thresholds

- Consider long-term implications for your insurance record

- Trust professional guidance over pressure tactics

GME's Commitment to Honest Service

Our promise:

- We'll tell you NOT to file when the damage is insufficient

- We'll support legitimate claims with full documentation

- We'll protect your insurance record like our own reputation

- We'll provide long-term solutions, not quick profits